The past months with Covid have of course been frightening and extraordinary. We're not through it yet, but we are starting to ask, what next, assuming things do get better and recover, as surely they must, how best to go forward, what lessons can be learned in a positive way, that can help organisations become smarter, better, more effective, perhaps more caring. Will this seismic shock result in a meaningful change to ways of working and ways of operating, will we avoid returning back to just the way we were, or can we find some new ways forward, ways which can better motivate our workforce, our stakeholders and our customers and perhaps deliver a more sustainable, and hopefully more resilient business model, a platform that can provide a better base for the future?

We are perhaps already seeing some green shoots. In China for example, there is a renewed momentum and recovery, and perhaps a gradual return to similar levels of output and production. Coal consumption which had fallen to 40% of 2019 levels is now back up to close to 80%. Real estate transactions, which had reduced to zero, are now back to 55% of 2019 levels. 94% of businesses have resumed operations. The official purchasing managers index has risen to 52 from February's record low of 35.7. Andy Rothman, an investment strategist with Matthews Asia, is seeing: " recovery underway and seeming to be picking up steam".

While we're still not over the worst, and the rest of the world yet to experience the kind of China bounce back, nevertheless, companies need to plan for the future and decide how best to move forward. Short term, that will involve re-budgeting and re-planning for 2021. There will inevitably be a high element of caution and conservatism, and much review of cash and working capital levels, perhaps significant reduced capex, working on scenarios which will likely assume a slow return to growth. More encouragingly, there has been some discussion about a stronger bounce-back, a "V-shaped" rebound. In the USA, Larry Kudlow, the Director of the National Economic Council, has said: "the economy could be reopened in the next four to eight weeks and would perform like a dynamo when it is". Treasury Secretary Steven Mnuchin has stated that he anticipates "a very strong rebound next year."

Too early to call, at the moment too much uncertainty, but can we nevertheless say that "things will never be the same again" and identify some key items that we can state with some certainty will change for the future, and for the better?

There are 4 things we can with perhaps put in that category:

Previously regarded as perhaps an employee occasional indulgence and privilege, but now become the "new normal" and likely to stay that way. And why not, internet connectivity can work from home or other remote location just as well as in the office. So why require people to travel to work every day, spend all that time commuting, increasing the carbon footprint, when they can just as easily do their work remotely, engage and converse and interact with ease and efficiency and with only the occasional need for face to face and in-person meetings.

There are now a plethora of video and document applications which make remote working reliable. We have read a lot recently about Zoom video conference and document sharing and collaboration tools and there are others such as Slack, Group Face Time on Apple, Google Hang Outs, Blue Jeans, Webex, Microsoft Skype and Teams…so plenty of low cost communication options.

Research also has shown that remote working can be much more productive. A Harvard Business School study over two years across a number of US organisations found increases in productivity of up to 13%, with employees saying: "easier to do my job", "more comfortable work environment", "reduced stress, so fewer sick days", "less distraction at the water cooler". In addition, the reduction in commuting occasions led to cost savings with reduced spend on transport to boost net income levels.

Transport emissions account for 21% of carbon footprint, and every day, employees have spent million hours commuting. One study found that 78% of a person's carbon emissions were due to their daily commute. For example, Xerox have claimed that by allowing 8,000 employees to do their jobs from home full time through its Virtual Workforce Programme, they saved 40,894 metric tons of greenhouse gases, amounting to around 5.1 tons per person.

Not everyone can work remotely of course but a new study reported in Forbes suggests that c. 57% of the US workforce could effectively work remotely either all or most of the time.

Here's a case study from Paul Judge, the Managing Director of a Management Buy-out of Premier Brands from Cadbury. It's from a few years ago but just as relevant and this is how a crisis helped drive better collaboration:

"At first, it was crisis time, we had completed the MBO from Cadbury, we had huge amounts of debt, limited working capital, customers cancelling, we didn't know what to fix first. It was like we were in a sinking lifeboat, water was leaking in on all sides, there was no time to discuss and debate what we should do, we were all totally united on one thing, save the boat! So it was all hands to the deck, 24/7 all single-mindedly focussed on the same goal. Looking back it was amazingly hard work, we were exhausted but it did also become exhilarating as the boat began to stabilise, we could see we were making progress and we felt we were actually going not only to survive but to flourish.

Looking back we had this unique spirit, all aligned, fix the problem, cut through the debate, find the quick fix, get things done, make it happen fast. After a while all that began to pay off, we could see land ahead.

And that is when the problems started, as soon as we had got to a solid and reasonably safe platform, we started to argue about what next! What direction should we go in, who should be responsible for what, what new equipment we should buy to start building our boat for the future? Progress started to slow. Decision-making which had taken seconds now started to take weeks. And after about 12 months, we noticed just how much things were changing.

While we had that crisis, that "burning platform" things were easy, relatively. Without that we had to find new ways to energise and engage everyone in our continuing journey, try to capitalise on the learnings of moving quickly, embed that somehow in our business as usual"

-case study from Paul Judge (who later helped establish the Judge Business School in Cambridge University), and who as the Managing Director, led the buy-out from Cadbury's of their former snacks /biscuits division called Premier Brands.

Four years after that historic management buy-out, the business was very successfully sold. Paul Judge went on to say that they never forgot those early crisis/burning platforms lessons. "we were always comparing things like speed of decision-making, how well and effectively we collaborated, the removal of silos in how we organised teams and projects…it stayed with us and was a key reason behind our subsequent growth and return to profit".

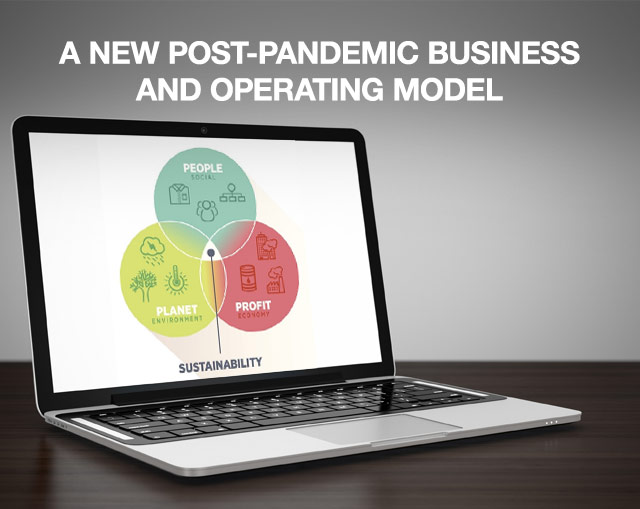

The triple bottom line framework (People, Planet, Profit), the "3Ps", was devised by a Professor John Elkington of University College, London. It's a framework that has never been more relevant than in today's complex, worrisome and fast-changing environment and as organisations think through their future ways of operating.

The challenge is for the whole model of business to adopt this new way of thinking and behaving, to report on these 3Ps with equal measure and emphasis, to show how each element is reinforcing the other to create a virtuous circle. It should no longer be enough to talk just about shareholder value and to justify all corporate behaviours along that line. Yes, it will always remain critical, but surely it can no longer be seen in isolation. And more importantly, it should be evaluated alongside and with equal weight to the impact on the other Ps of People and Planet.

It might for example be the lowest cost, best shareholder value solution to build a new factory in a low cost low regulation environment. But if that might lead to higher emissions, or more carbon footprint or damage to the planet then that can no longer be the right answer. Investing shareholders have to accept this "new normal", that the optimal solution may not be the lowest cost /highest Profit option.

Equally, corporate actions needs also to be judged alongside impact on the workforce, on customers, on users, on people. Does this initiative help or harm, does it empower and enable, does it help work:life balance rather than reduce or harm it? What more can an organisation do for gender and ethnic diversity, how can we help people who are disabled or disadvantaged, how can an organisation help its local communities and stakeholders?

A more responsible approach to business is now being called for. We've seen a coming together of these sort of 3P ideals in the past weeks as companies work to respond to the virus pandemic. We've seen companies take steps to protect their people and we must hope that this more vigorous People concern will grow and endure and not get forgotten.

As we enter perhaps a new era in company organisation and thinking, and with the expected new norm around remote working, we should ask if there's a need in the future for so much office space?

We work in a world where technology is changing our lives, fast and everyday, the old-fashioned idea of having to frequently be in the same building to do the job is becoming out-moded, as we have all seen how we can connect just as easily from anywhere. So all this office space surely just not required.

We can draw parallels from the world of retail. Technology has enabled online shopping for the past 20 plus years. Retailers could see the shift, how tech was changing the game, how in the future they would not need so many shops. But most retailers ignored the warning signs, kept opening new shops, investing in new space, convinced that what happened with books and CDs and DVDs would never happen to them. But of course the march of technology has continued at pace, inexorably, and now there's a retail /high street crisis. Retailers are stuck with too much space, they failed to adapt their business model, even though they had years of warning.

So with commercial offices, Amazon and Google for example are even now building vast new offices for all their staff. Even though they acknowledge the opportunity for remote working, so they still believe they need office space on the principle we need physical space for everyone. But they too will surely soon realise that is an antiquated idea. Some flexible space in WeWork for occasional meetings is all that's required.

This virus pandemic has highlighted yet another new imperative, don't invest in commercial office real-estate, companies with large physical office portfolios will soon find they're stuck with costs and assets they just don't need anymore.

One thing is clear: we can't go back to a 20th century business and operating model. Time has moved on, things will never be the same again.

From the MTV nominated best song by Mel C of the Spice Girls:

Things will never be the same again

It's just the beginning it's not the end

Things will never be the same again

It's not a secret anymore

Now we've opened up the door

Starting tonight and from now on

We'll never, never be the same again

"You must be the change you wish to see in the world."

-Mahatma Gandhi

© Michael de Kare-Silver 2024

Michael runs this specialist and international recruiting /headhunting practice Digital 360, helping companies recruit key talent where Digital Tech and /or Data skills and savvy are important.

Michael used to be MD at Argos.co.uk and of Experian.com, he is ex McKinsey strategy consulting and Procter & Gamble marketing, Michael provides a personal and dedicated advisory and recruitment service that delivers results and is built on treating people with kindness and respect.